3rd EUROPEAN MINING & EXPLORATION FORUM

Sustainable development of the Western Tethyan metallogenic resources

MINEX Europe 2018

Balkan Mining Investment

Balkan Mining Investment

High-level MINEX Europe Conference in Macedonia Indicates Growing Interest in Balkan Mining Investment By Chris Deliso From June 12-14, Skopje hosted the MINEX Europe 2018 conference, bringing together leaders in government, the mining industry, finance, science,…

Read more Event materials

Event materials

The online version of the Forum materials will be available from 29 June 2018 and will include: Slides presented during the Forum (in PDF) Forum catalog with information about presenters, sponsors, and exhibitors (PDF) Video…

Read more MINEX Europe report

MINEX Europe report

The 3rd MINEX Europe Mining & Exploration Forum was held in Skopje, the Republic of Macedonia, on 12-14 June 2018 under the theme “Sustainable development of the Western Tethyan metallogenic resources”. From high-grade development projects…

Read more

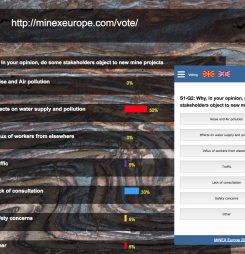

Survey Results

What are the key challenges for sustainable development of the mining projects in Central and Eastern Europe? Is there are future for mining in Europe’s future Circular Economy? What companies and Government should do to…

Read more MINEX Europe photos

MINEX Europe photos

Over 200 delegates attended the opening session of the Forum. Deputy Prime Minister Mr Kocho Angjushev spoke about extensive opportunities for unlocking the country's mineral potential and called on the delegates to discuss the ways…

Read more Meet mining companies

Meet mining companies

The Forum will provide the platform for meeting senior executives from over 20 mining companies operating projects in the countries across the Tethyan Belt. Macedonia: Central Asia Metals, Euromax Resources, Sardic, Reservoir Minerals, Genesis Resources,…

Read more SRK workshop

SRK workshop

Effective and safe disposal of mine wastes presents significant environmental and technical challenges to mining operators worldwide. On 13 June SRK Consulting (UK) Ltd will be running the workshop on Mining Waste management. This workshop…

Read more Buchim Mine site visit

Buchim Mine site visit

On 14 June the Forum delegates will be able to visit Buchim Mine operated by Solway Group. The construction of the Buchim mine, located in Southeastern Macedonia, began in 1976 and the plant became operational…

Read more Why Western Tethys?

Why Western Tethys?

With Euromax Resources looking to develop the Ilovitza gold project, Solway Group’s Bucim copper/gold mine, Genesis Resources Plavica gold project at feasibility and the recent $400m purchase of the Sasa zinc project by Central Asian…

Read more Forum announcement

Forum announcement

Preparations for the 3rd MINEX Europe Mining & Exploration Forum have begun. The Forum will be held in Skopje, the Republic of Macedonia on 12-14 June 2018 under the theme “Sustainable development of the Western Tethyan…

Read more Call for speakers

Call for speakers

MINEX Europe Technical Committee calls on national and international mining companies, analysts, investors, technological companies and government authorities to submit before 1 May abstracts to be considered for presentation at the Forum. The Forum agenda and confirmed speakers…

Read more Early bird discount

Early bird discount

Delegate participation Local and international companies whose professional interests are aligned with the Mining development of Western Tethyan regions and across European Continent are cordially invited to participate in the Forum’s meetings which will shape…

Read more MINEX Forum News

MINEX Forum News

Stay up-to-day with headlines and exclusive news. Subscribe to the MINEX Forum Eurasian Mining weekly updates here About MINEXForum online platform MINEX Forum TM is a specialist events and information exchange platform dedicated to Mining Technological Innovation, Regulation and…

Read more Mining Project panels highlighting projects development across Balkans, Bulgaria, Turkey, Caucasus and Central Asia.

Mining Project panels highlighting projects development across Balkans, Bulgaria, Turkey, Caucasus and Central Asia.

Trade show innovation trends for exploration and extraction, processing, waste management, and reconciliation

Trade show innovation trends for exploration and extraction, processing, waste management, and reconciliation

MineTech Europe mining innovation and challenges competition

MineTech Europe mining innovation and challenges competition

“The Circular Economy and Sustainability in Mining” round table

“The Circular Economy and Sustainability in Mining” round table

Day trips to mine sites operated by the Macedonian and International companies

Day trips to mine sites operated by the Macedonian and International companies

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}